Imputed income has become a crucial factor that adds the value of fringe benefits to income. It has been harnessed to nullify the wastage of the firm’s resources and perks.

Although the provisions regarding it have been mentioned in multiple local laws, several rumors and myths have mounted around it, diluting its actual meaning and purpose. Further, its resemblance to other similar concepts has tangled its essence.

To answer what is imputed income, here we have holistically explored and discussed every single dimension of this concept in this blog to exhibit the most accurate and authentic information to you.

What is Imputed Income?

Imputed income is the cash value of the non-salaried benefits that employees get from the employer. It is combined and credited to the employee’s gross income.

The root word of this term, i.e., “impute,” has a fundamental meaning in finance, which is estimating the value of something where the actual price is precisely not known or derived.

In US corporate culture, it is added to the gross income of the employee and is reported in the W-2 form, tax, and wage statement.

Another similar concept deeply interwoven with it is the domestic partner’s imputed income.

What is the Domestic Partner’s Imputed Income?

Domestic Partner’s imputed income is the income received against the benefits that the employer provides to the domestic partner of the employee. The domestic partner is not the spouse or a legal dependent. As the domestic partners are not considered spouses, benefits offered to them are generally taxable.

However, in certain cases, the financial interdependence is considered for such purposes, which are subject to the prevailing laws and rules.

But you might be wondering which benefits are included while calculating the imputed income.

Here are some examples.

10 Most Common Examples of Imputed Income

The imputed income is derived by considering certain additional perks beyond the regular salary. These are called fringe benefits, which are provided by the employer to the employee to attract and retain the best talent in the firm.

From the imputed income’s point of view, here are some of these benefits, which are estimated to add their value to the gross income.

- Meals

- Gym memberships and athletic facilities

- Transportation benefits.

- Tuition reduction

- Cellphone provided by the employer

- Medical facilities

- Working conditions benefits

- Educational benefits

- Retirement planning services

- Employee discount

Some other benefits are also there in the list, which vary from firm to firm and are added selectively by the employer.

Besides, some perks are excluded from this list and are not considered which impact the imputed income definition.

What is Excluded from Imputed Income?

Some provisions are to be excluded while calculating the imputed income. They are generally mentioned and reasoned in the laws and regulations.

Here are some benefits provided by the employer to its employees that are excluded.

- Health insurance for the dependents

- Care assistance for the dependents is less than $5000

- Merchandise for the employer, such as t-shirts

- Health savings account

- Adoption assistance

- Education assistance below a limit

- Occasional meals

- Group term life insurance (under certain conditions)

- Gifts from the firm, such as gift cards and movie tickets

These provisions differ from country to country based on the enacted laws and regulations for the corporate sector. They determine which benefit is to be included and which is to be excluded.

Now let’s clarify the difference between the two very similar concepts, i.e., imputed income and fringe benefits.

Difference Between Imputed Income and Fringe Benefits

Imputed income and fringe benefits are interrelated, as fringe benefits are valued while calculating the imputed income.

The fringe benefits are the non-cash benefits that the employer offers to the employee, while the taxable part of the monetized non-cash benefits refers to the imputed income. This relation has been presented in the following infographic to depict the crux.

To understand the terms better, here is a table exhibiting the difference between their major features.

| Feature | Imputed Income | Fringe Benefits |

| Definition | Taxable value of fringe benefits | Non-cash benefits provided by a firm to its employees. |

| Purpose | To calculate taxable income | To attract good talent |

| Taxability | It is always taxable | Not entirely taxable |

| Example | Fair market value of the gym membership | Gym Membership |

After exploring all related facets of imputed income, the next doubt popping into your mind would be how imputed income is calculated.

Let’s address it in the subsequent section.

How is Imputed Income Calculated?

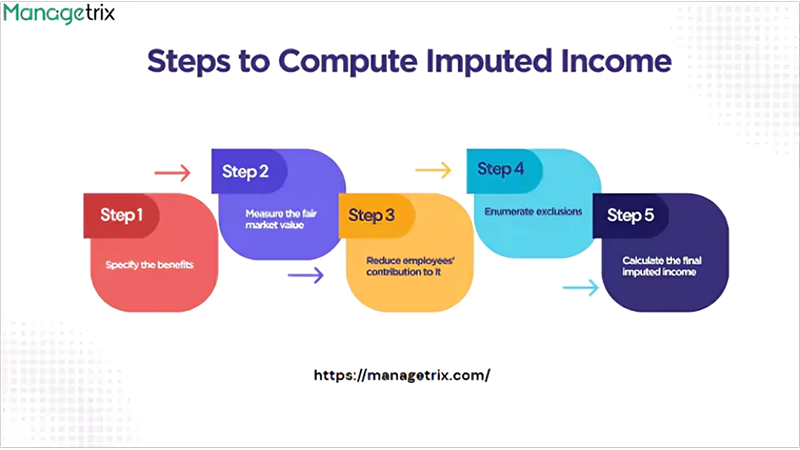

Imputed income is calculated by estimating the fair market value of the fringe benefits. The bona fide process to calculate the imputed income has immense technicalities and rests as one of the responsibilities of HR. However, we have mentioned it below through infographics and in succinct steps to help you understand it better.

- Specify the Benefit: Identify the fringe benefits that the employer is providing. Make sure they are included in the local income tax laws.

- Measure the Fair Market Value: Evaluate the fair market value based on the prevailing rates.

- Reduce Employees’ Contribution to it: In case the employee has paid for any part of the cost of the benefit, subtract this amount from the fair market value.

- Enumerate Exclusions: Some benefits are excluded from being calculated as imputed income, while some have been put under a threshold as mandated by the local tax laws. These need to be calculated before reaching the imputed income.

- Calculate the Final Imputed Income: After reckoning all the benefits, a gross payment figure is arrived at, which is the final imputed income and is to be credited to the taxable salary of the employee.

A firm’s HR reports can show the imputed income by adding the calculated value to the employee’s W-2 form (a tax statement in the US) and furthering the process under the prevailing regulations.

Some firms have included it in their salary slip format to bring more transparency and authenticity.

Although the concept has been made clear, some of you might doubt imputed income life insurance, which is sometimes considered a taxable part. However, it generally happens in certain conditions, which are discussed in the following section.

What is Imputed Income Life Insurance?

Imputed Income Life Insurance is a threshold of worth of life insurance, beyond which its value is considered imputed income and is taxed.

As the imputed income is calculated from the fringe benefits such as gym memberships, commuting services, etc, some of them also incur significant tax liabilities to the employee.

Some firms provide life insurance to their staff members as a perk. Considering general term life insurance, the IRS (Internal Revenue Service) accounts for coverage beyond $50,000 as imputable income and is thus lawfully taxed. This means that this extra coverage will appear on the W-2 form.

However, some factors play a significant role in this perspective.

- When the employee pays any part of the premium, their taxable amount will be reduced.

- If the employer pays the entire premium, the taxable amount will be based on the employee’s age and the IRS premium table.

The table below will help you further calculate the excess taxable income.

| Employee’s Age | Taxable Income Cost per $1,000 of Excess Coverage |

| Below 25 | $0.05 |

| 25-29 | $0.06 |

| 30-34 | $0.08 |

| 35-39 | $0.09 |

| 40-44 | $0.10 |

| 45-49 | $0.15 |

| 50-54 | $0.23 |

| 55-59 | $0.43 |

| 60-64 | $0.66 |

| 65-69 | $1.27 |

| 70 or + | $2.06 |

In case you are paying the premium of general term life insurance offered by your firm, you must consider this table to ensure your eligibility for the imputed income benefits.

Conclusion

The above discussion is sufficient to understand what imputed income is. These provisions vary from nation to nation, depending on the prevalent corporate laws, rules, compliances, and policies, for which having a detailed analysis of the same and a genuine guide is highly advised.

Hence, the entire information at your disposal is beneficial in calculating it and measuring its impact on your gross income.

FAQs

1. What is the imputed income meaning?

Ans: The meaning of imputed income is the part of the salary that the employee receives after surrendering the non-cash service benefits provided by the employer.

2. How do you calculate imputed income?

Ans: Imputed income can be calculated by identifying the fringe benefits, subtracting the exclusions, calculating the fair market value of the benefits, and deriving the net outcome.

3. What is the imputed value?

Ans: Imputed value is the estimated value of something when the actual price or value is not known. It is derived by using the fair market value of the items.

4. What is an example of a fringe benefit?

Ans: Vacation benefits, health and life insurance, pension plans, gym, and sports club membership, etc., are some examples of fringe benefits.

5. What does fringe benefits mean?

Ans: It means the non-wage benefits that an employer offers to the employee to attract and retain good talent in the firm.

6. What is Section 125 cafeteria plan?

Ans: The cafeteria plan is a framework of the business to provide perks to the employees. This provides tax advantages to the employee as well as the employer.

{kind=link}